Matching Your Assets to Your Needs

As a financial advisor located in Greeneville, TN, I am frequently asked which assets to invest in. One of the most important decisions investors make is deciding which assets to invest in. These can have a significant impact on the overall performance of your portfolio. So, choosing investments that don’t match your needs or goals can prove self-defeating (or downright disastrous) over time.

Significant losses and overall financial instability sometimes accompany mismatched assets like fire accompanies smoke. That’s why this article explores how people may stumble into this crucial mistake. With these missteps in mind, we suggest ways to help you avoid them.

This article discusses these topics:

- Why match assets with your needs?

- The risks of mismatching assets

- How to match assets to your needs

- Get better at investing with Sapiat

Why Match Assets With Your Needs?

Unfortunately, we’ve noticed some investors mismatching assets to their needs. It often causes them both financial instability and, usually, market losses. I’d love to tell you that it’s gotten rarer due to today’s inflation and stock market uncertainty, but it hasn’t. The problem has actually grown worse and worse over the past 2-3 years.

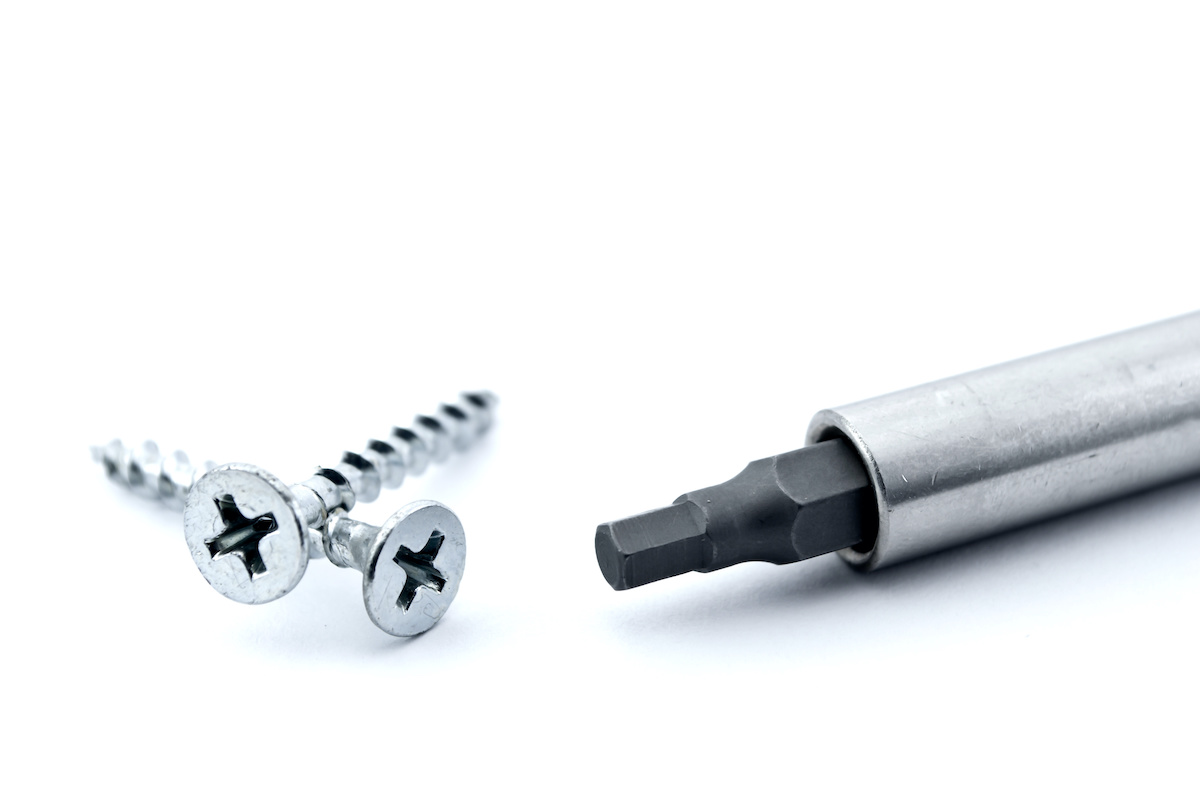

Whenever we discuss it, I ask clients, “Which is a better tool, an axe or a wrench?”

If someone says, “An axe,” I’ll ask, “What if I told you the job you need it for is tightening some bolts?”

If they say “A wrench,” I ask them, “What if the job is splitting firewood?”

Alternatively, I may ask them which is the better vehicle between a new John Deere tractor or a new Mercedes-Benz. In either case, the point is the same: Investing, fundamentally, is about selecting the right tools, meaning the right assets, for the job at hand. Just as you wouldn’t snatch up the axe to open a city water valve, rushing into the wrong investments can leave you ill-prepared to get anything significant done.

Sapiat is a financial planning and asset management firm. We do financial planning in Greeneville, TN. Connect with us today for a more secure tomorrow!

The problem with this is that—unless you hold a lot of short-term assets, specifically for this kind of thing—it’s hard (if not impossible) to succeed as an investor this way. Assets in your portfolio are there for playing the long game. It shouldn’t be an entirely set-it-and-forget-it situation, which is why we periodically rebalance them.

However, you can’t win the football game, as an investor, by pulling players off your bench to rake leaves in the parking lot, either. The equity you’ve invested into your assets; your players, have to stay on the field until the game officially ends. Your immediate, pay-the-bills financial needs, meanwhile, should be addressed with cash on hand at the (real) bank.

If you try to use your market investments for short-term goals, you’re almost certain to lose the game in one way or another. In the simplest terms:

- Investments are for your long-term goals.

- Cash is for your short-term goals and emergencies.

As an investor, you have different needs and goals than other people do. Understanding your unique needs and goals is critical when selecting assets to invest in. It’s a first step you literally can’t afford to skip.

The Risks of Mismatching Assets

Failing to properly line up your assets with your specific financial needs as an investor may diminish your nest egg. Again, cash is for immediate needs and emergencies. It doesn’t earn enough interest to match (much less beat) inflation.

Thus, the cost of the goal increases faster than the value of the asset. Over time, this gap widens further, reaching enormous proportions. That’s why relying on cash to reach mid- and long-term objectives often causes people to fall short of their financial goals.

Fixed income assets (such as bonds and fixed annuities), meanwhile, are for immediate income needs or short-term goals. Most of these assets; maybe even all of them, have some sort of penalty or market value adjustment. This causes their value to drop precipitously if they’re sold or surrendered early. As a result, you could lose all of your earnings and potentially, some of your principal.

Unless an investor pays careful enough attention to match maturity dates with their time horizon, using fixed-income assets to pay for large future expenses can also cause an investor to come up short of payment for their goal. Most fixed-income earnings only match inflation. So, if all of your earnings are consumed as income, the purchasing power of your principal falls over time.

Your equity is best reserved for mid- and long-term goals. Part of the reason why is that it can be volatile in the short term (though volatility usually levels out over time). So, using equity to fund a short-term goal is a recipe for failure, since the equity asset may experience a large, temporary drop in value during short time periods.

Keep an eye on your asset mix; your cash, fixed income, and equity. These should slowly change over time as your needs/goals, time horizons, and market conditions vary. Making sudden shifts in your asset allocation, which ignore these factors, is asking for trouble.

For example, if you decide to go from a focus on equity to fixed income at retirement, we should map out possible ramifications together, first. Retirement is a long-term goal that often lasts 20-40 years. So, to protect your nest egg, the shift away from equity should be done very gradually.

There’s an Art and a Science to Investing When Inflation Is So High. Read More Here.

How To Match Assets to Your Needs

As promised, I’m offering possible solutions. Matching assets to your needs should always start with carefully considering your financial goals and investment time horizon.

To show you what this looks like, here are some steps to follow:

- Define Your Goals. Start by defining your investment goals. Are you looking for long-term growth? Or, maybe, a steady income stream?

- Consider Your Time Horizon. Your time horizon is also essential when selecting assets. Are you investing for the short term or the long term?

- Diversify Your Portfolio. Finally, diversify your portfolio. Investing in a variety of assets can help you manage risk and achieve your investment goals.

Get Better at Investing With Sapiat

Especially with a recession likely this year, now is a wise time to ensure your financial plan is market-weather-ready.

Especially with a recession likely this year, now is a wise time to ensure your financial plan is market-weather-ready.

Sapiat Asset Management provides comprehensive financial planning in Tennessee.

We also invest in our clients by encouraging them to grow their financial literacy. The better you understand the financial world around you, the more you can make well-informed decisions as an investor.

Action Items

- Don’t Quit. Quitters never win.

- Minimize Your Withdrawals. Reduce or suspend them to help your portfolio recover quicker when markets turn around.

- Buy Low. The 2023 limit is $22,500 (or $30,000 if you’re age 50 or older). Max your IRA/Roth contributions, as well. The 2023 limit is $6,500 (or $7,500 if you’re age 50 or older). Consider temporarily increasing your 401(k) contributions while you’re at it.

- Plan for economic uncertainty. In other words, update your financial plan ahead of the need now, before more storms arrive. If you don’t have a roadmap to update, call us to get started ASAP.

To counter inflation and rising interest rates:

- Minimize fixed-income assets and cash. CDs, cash, bonds, and fixed annuities all lose purchasing power when inflation is high.

- Thin out fixed-income investments. Bond values go down when interest rates rise (because floating-rate assets gain).

- Reduce any variable-rate debt. Pay off or at least pay down any variable-rate debt before your rates go higher.

If you’ve never worked with a wealth manager before, we’re ready to be your Greeneville, TN, financial advisor. Contact Sapiat to learn more about our fee-only financial services, tax planning, and more.